The banks are same-sameish in a lot of ways.

Take mortgage interest rates, for instance, where chances are you’re going to get more or less the same rate no matter where you go.

But there’s one aspect of your banking where there can be major variation from bank to bank. And that’s your savings account.

In this article, we’ll take a look at all the different options on offer across New Zealand’s main retail banks — and how they stack up against each other.

Choosing a savings account usually means having to pick between earning great returns or having easy access to your money. You can’t often have both.

Generally, the longer you can commit to locking funds away for, the more interest you’re going to earn on them. But you won’t want your savings tied up in 5-year term deposit, earning top rates, if you think you’ll need to dip into them in a few months’ time.

What’s right for you will depend on your savings goals — and the banks have a whole raft of account options that span the full spectrum.

The major perk with a standard savings account is that your money’s on-call, so you’re free to withdraw it any time you like. But not all savings accounts are created equal.

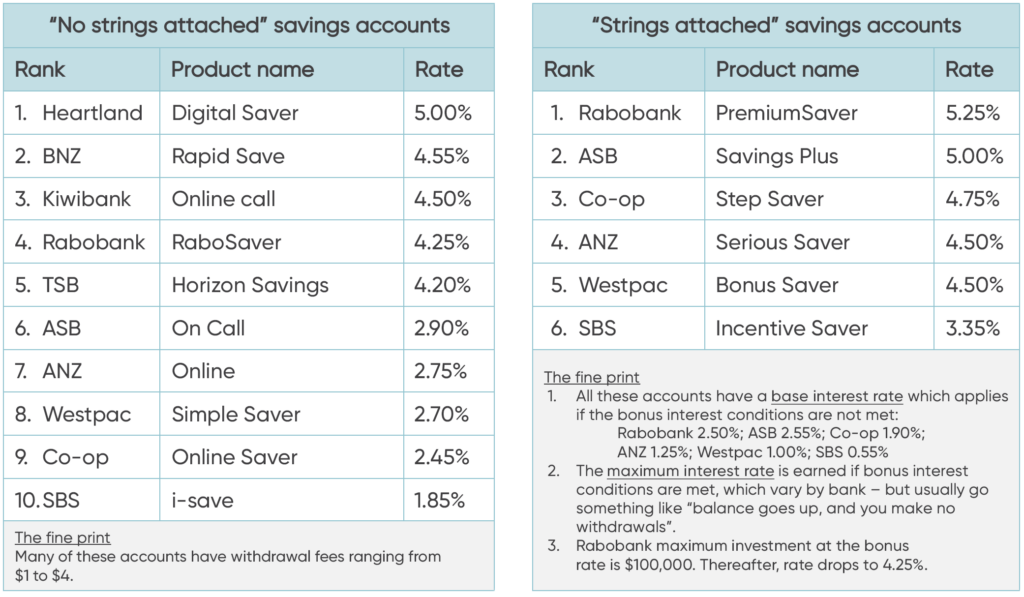

There are two main types of account on offer — some with strings, and some without.

1. No strings attached

These savings accounts are as stock-standard as they come. You earn a single, flat interest rate – accrued daily and paid monthly — which won’t change based on your account activity.

These accounts do often carry transaction fees for withdrawals, but you usually get the first withdrawal you make each month free-of-charge.

2. Strings attached

A few of the banks have another option where you can earn a higher interest rate, but you’ll have to jump through a few hoops to get it. The conditions you need to meet vary by lender, but usually go something like “balance goes up, and you make no withdrawals”.

If your bank offers a “strings attached” account (not all do) and you’re confident you can meet all the conditions, you’ll earn a better rate than you would with their “no-strings” account. But if you don’t meet all the rules, the return will be woeful.

There are 10 main retail banks in New Zealand, and here are the best savings accounts on offer from each across these two categories.

If you know you won’t need your money back at short notice, or you’re happy to just lock it away for a year or five, you’ll be able to earn a lot more interest.

And again, there are a couple of different options.

1. Notice Saver accounts

The clue’s in the name with this one. Notice saver accounts still let you take your money out without penalty, but you’ve got to give the banks plenty of advance notice before doing so. Either 32, 60 or 90 days, depending on the account.

Kiwibank, Heartland, Rabobank and Westpac are currently the only banks that offer Notice Saver accounts — and they pay interest rates anywhere from 4.75% to 5.75% depending on the bank, and the notice term.

2. Term Investments (a.k.a. term deposits)

With a term investment, you’re choosing to lock your money away for anywhere between 30 days to 5 years.

The major difference between this and a notice saver account is that if you need your money out before the term is up, you’re going to have to pay the price of lower (or no) interest.

Right now across New Zealand’s major retail banks, interest rates on 30 to 90 day terms range from 2.40% to 4.20%.

Once you get up to terms of six months and beyond, you’re looking at over 5.00% returns — but you’ll want to be confident that you won’t need that money back before term.

A relatively recent addition to New Zealand’s suite of savings products, the Squirrel On-Call account is built different.

It currently pays 5.25% p.a.* with no strings attached — so you don’t have to compromise on either earning a solid rate or having easy access to your funds.

Funds can be moved between your main bank and Squirrel (and vice versa) within two hours, 7 days a week, as long as you make the transfer between 9:00am and 10:00pm.

And every cent of your money is held on trust in an account with a Standard & Poor’s AA- rated major registered bank. So it’s like having your money in a regular savings account, just with better returns.

You can find out more about the Squirrel On-Call account on our website, or…

*Interest rates accurate as at 11 April 2024.

**Please note the interest rates referenced in this article are “gross rates” i.e. before the deduction of any applicable withholding taxes.

The opinions expressed in this article should not be taken as financial advice, or a recommendation of any financial product. Squirrel shall not be liable or responsible for any information, omissions, or errors present. Any commentary provided are the personal views of the author and are not necessarily representative of the views and opinions of Squirrel. We recommend seeking professional investment and/or mortgage advice before taking any action.

To view Squrrel’s disclosure statements and other legal information, please visit our Legal Agreements page here.

Deposit Rates will occasionally send out email newsletters with the latest news, rates updates and special offers.

Disclaimer – Every possible effort has been made to keep the information in the tables and on this site as accurate as possible, however, neither the publisher, Tarawera Publishing, nor anyone engaged to compile the rates and this site accept any liability for inaccuracies or any loss suffered as a result. It is strongly advised that readers check loan details with providers. The full terms and conditions of this site can be found here.